(B)(N) VZ Verizon Communications Incorporated

Deal Book. Verizon Communications Incorporated was formed in 1999 with the merger of Vodafone PLC’s U.S. wireless assets and the Bell Atlantic Corporation, and Vodafone continues to own 45% of Verizon, and is itself also the second-largest mobile telecommunications provider in the world, operating in over seventy countries (often with local partners), and trailing only China Mobile in terms of revenues and subscribers. Verizon, apparently, has offered $100 billion in a 50:50 cash and stock deal to repatriate Vodafone’s interest to itself, but a major block of Vodafone shareholders, constituting about 25% of the outstanding stock, has said that $100 billion is not enough – they want more such as between $120 billion and $135 billion, whereas the entire market value of Vodafone is $150 billion on a good day, and absent its interest in Verizon, the “street” says $10 billion might cover it (Reuters, April 26, 2013, Vodafone investors want bigger bid or full takeover by Verizon)

However, they are open to Verizon taking over Vodafone (for some reason), so let’s look at that: Verizon buys Vodafone, reconstitutes itself, and acquires a global network. And the Vodafone shareholders acquire cash plus new Verizon stock issued from the treasury stock at no par value.

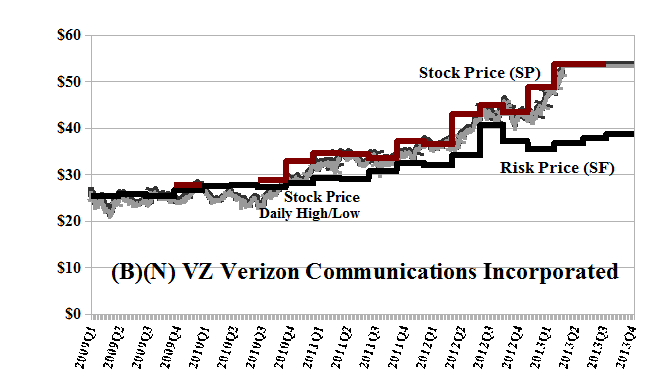

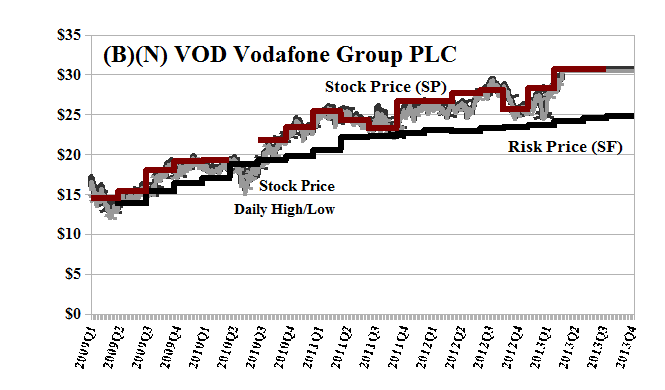

The risk price for Verizon is currently $39 so that the risk-adjusted value of Verizon is $39×2.858 billion shares = $110 billion, 45% of which is owned by Vodafone, and the risk-adjusted value of Vodafone is $25×4.965 billion shares = $123 billion (please see Exhibits 1 and 2 below). The “common interest” is therefore “worth” 45% of $110 billion which is $50 billion equivalent to cash in round numbers, and leaves a risk-adjusted value of $73 billion for the rest of Vodafone and $60 billion for Verizon; however, we’re not buying the “common interest” in Verizon from Vodafone – we’re buying all of Vodafone, and the “common interest” comes with it.

The current market value of Verizon is $153 billion and of Vodafone, $152 billion, so that one Verizon share is worth (153/110)/(152/123) = 1.13 Vodafone shares at the market price of the risk that they carry and there are 4.965 billion of those, and it doesn’t matter who owns them – they’ll all be converted to Verizon stock as equivalent to cash. An all stock transaction would therefore require 4.965/1.13 = 4.41 billion shares of Verizon stock to acquire all the shares of Vodafone with a current market value $152 billion for which Verizon would offer 4.41 billion new shares, newly minted out of treasury and valued at the risk price of $39 (and not the market price of $54) and therefore, worth $172 billion, as good as cash. No other cash is required, and we’ve thrown in a bonus of $20 billion, thank you very much for doing this deal and helping us to implement it. Welcome to Verizon. (If Verizon wants to use some “cash”, they should just buy in some Vodafone stock at the market price once the deal is announced or up to 10% of it before the deal is announced, and their shares will be treated just as the others.)

Why does this work? Can the shareholders and boards of directors understand it, and feel good about it? Why is it a win-win-win situation? Vodafone is gone, but Verizon is still substantially owned by the ex-shareholders of Vodafone, who are now just the common shareholders of Verizon and own 4.410/(4.410+2.858) = 60% of the combined company should they continue to vote as a block, which is unlikely because Vodafone has many other shareholders as well as the “block” that controlled 25% of Vodafone’s stock and now controls just 15% of Verizon’s stock as a “block”.

Moreover, it’s evident that Verizon’s original offer – $100 billion cash and stock – was crafted to sound good but is no better than the wind that carries it, and that the Vodafone shareholders were much closer to understanding the worth of their stake and company. It’s too easy to get tangled up with egos and “market values”, demonstrated or projected, so we reduced all of the data to the one thing that everybody understands – cash. The only issue is why is Verizon worth $110 billion as cash, and why is Vodafone worth $123 billion as cash when their market values are calculated using their “price of risk”, the Risk Price (SF) of $39 and $25, respectively, rather than their stock prices of $54 and $31, respectively.

The key word is “as good as cash”. We can expect no more from cash, other than that it will retain its face value (but not its purchasing power), which we do here in terms of the common stock of public equities as demonstrated by the “cash” which the investors are willing to forgo – regardless of inflation – in order to buy and hold the stock at the current market prices relative to the “price of risk”. That’s it. Please see below for additional references.

Exhibit 1: (B)(N) VZ Verizon Communications Incorporated – Risk Price Chart

(B)(N) VZ Verizon Communications Incorporated – April 2013

Verizon Communications Incorporated is a provider of communications, information and entertainment products, and services to consumers, businesses and governmental agencies through its two business units, Verizon Wireless and Wireline.

(Please Click on the Chart to make it larger if required.)

Exhibit 2: (B)(N) VOD Vodafone Group PLC – Risk Price Chart

(B)(N) VOD Vodafone Group PLC – April 2013

Vodafone Group PLC is engaged in providing voice and data communications services for both consumers and enterprise customers, with a significant presence in Europe, the Middle East, Africa, the Asia Pacific region and the United States.

(Please Click on the Chart to make it larger if required.)

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation.

Stock prices that are less than the price of risk are “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”. On the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information, and therefore their interest is as good as, if not better than cash. Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more details, and for more on the “stock as cash at the risk price”, (B)(N) VRX Valeant Pharmaceuticals International, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

SOURCE Verizon Wireless