Guts, Glory, And A Good Story

Drama. The Wall Street Journal has used all of the best theories of investment prowess and business practice to identify nine of the biggest name-brand public companies traded in New York, that can’t get any bigger and, presumably, could get to be a lot “smaller” (The Wall Street Journal, April 5, 2013, Nine Famous Companies That Can’t Get Bigger). Nor is this news isolated or obscure – the Wall Street Journal is owned by the News Corporation which also owns the Dow Jones & Company, the Fox Broadcasting Company including the Fox Business Network, Fox Sports, and the Fox News Channel, and the New York Post, HarperCollins Publishing, and Twentieth Century Fox – and pulls no punches. Stuart Varney, Sean Hannity, Greta Van Susteren, and Bill O’Reilly, for example. Investor! Beware!

The Wall Street Journal has named names and found that the Sears Holding Corporation, Dell Incorporated, and Hewlett-Packard are “mismanaged” and “have been battered by superior competition” and that the remaining six, the Lockheed Martin Corporation, General Dynamics Corporation, Allstate, Safeway, Proctor & Gamble, and AT&T are better managed in challenging circumstances, but are “boxed in” by industries that are saturated with competition and slumping or limited demand.

And despite the pressure on their revenues, some of these companies are “making up for their lack of revenue growth” by supporting investors and the stock price (we don’t know why they would do that, absent a takeover price) with “share buybacks” or “dividend increases” with AT&T currently yielding 5%, Lockheed Martin 4.8%, and General Dynamics 3.3%, all of which are much better than the bond and interest rates.

This is sensational. But it doesn’t have anything to do with investment success. It’s just news and a fabulous display of investment jargon and scuttlebutt akin to entertainment, and so presented.

The average stock market return for these nine companies, with a total market capitalization of about $600 billion, is +12% in the last three months (please see Exhibit 1 and 2 below) and six of them are currently in the managed portfolio that we call the Perpetual Bond™ and their return in the last three months is +8% plus dividends (because we buy and hold whenever possible) and it will not be any less than that for the rest of the year.

Exhibit 1: The Wall Street Journal Tiny Tots – Portfolio Summary

The WSJ Tiny Tots – Portfolio Summary

(Please Click on the Chart to make it larger, and again, if required.)

Exhibit 2: The Wall Street Journal Tiny Tots – Cash Flow Summary

The WSJ Tiny Tots – Cash Flow Summary

(Please Click on the Chart to make it larger if required.)

Of these nine companies, some of them are rather easy to be wary of, and the Hewlett-Packard Company and Sears Holding Corporation have also made it to another notorious list (please see our Post, America’s Most Unwanted Companies, February 2013, also from The Wall Street Journal) and the future of Dell Incorporated is uncertain at the present time and none of them are in the Perpetual Bond™ but they have returned +42% (Hewlett-Packard), +15% (Sears) and +38% (Dell) which is not something that happened because of something that the companies – which appear to be hapless – did (please see our Post,(B)(N) DELL Dell Incorporated, February 2013, and The Dow (B)-Nots, April 2013, for other situations).

On the positive side, please see our recent Post on (B)(N) PG Proctor & Gamble Company, April 2013, and AT& T in (B)(N) DISH Network Corporation, April 2013, both of which are in the Perpetual Bond™ now and up +18% and +12% so far this year.

We discuss the situation of Allstate (+21%), Safeway (+47%), General Dynamics (-5% and the only loser of the six that are in the Perpetual Bond™, although it has struggled from $50 to $70 in the last few years; please see Exhibit 5 below), and Lockheed Martin (+3%) below (Exhibits 3 through 6) and we will also need to struggle – to understand the difference between news and information that might affect our investments.

Exhibit 3: (B)(N) ALL Allstate Corporation – Risk Price Chart

Allstate is a $23 billion company that pays shareholders a dividend of $470 million per year with a current yield of 2%. It is trading well above the current Risk Price (SF) of $35 and although we can afford the stop/loss price of $44 out of our profits, we can also consider options as a “collar” to protect our current price of $48 to $50. For example, the January 2014 put at $48 costs $3.05 today and the cost of that can be partially offset with a sold or short call at $50 against our long position for $2.70 today, so that for a net cost of $0.35 per share ($3.05 less $2.70), we can collect our dividends and protect our price between $48 and $50 for the rest of the year.

Allstate has been substantially in the Perpetual Bond™ since prices of $20 in 2009 (please see Exhibit 3 below) but a recent report by the research firm, Zacks Investment Research, has advised us that “Allstate’s top-line growth slowed due to increased competition that includes the giant insurers Geico and Progressive, and it is difficult for any of them to raise rates as they hold one another in a competitive check to hold on to their customers. This means that the relatively flat revenue the company has posted in the past eight years will continue.” – ibid, The Wall Street Journal.

And, hopefully, from our point of view, inspire an increase in their stock price by another 100% in the next four years of eight.

(B)(N) ALL Allstate Corporation – Risk Price Chart – April 2013

Allstate Corporation is the holding company for the Allstate Insurance Company which offers personal property and casualty insurance, life insurance, retirement and investment products.

(Please Click on the Chart to make it larger if required.)

But, alas, none from The RiskWerk Company, which is a shame and a problem for them, considering that their investment products are insured products such as segregated funds, and they also need to obtain superior returns in their bond and equity portfolios in order to afford lower insurance rates and better annuity returns for their customers and to improve their competitive position.

Exhibit 4: (B)(N) SWY Safeway Incorporated – Risk Price Chart

The Safeway Incorporated stock plunged (-15%) yesterday (April 25) from $28 to $23 with a trading volume of 25 million shares, which is more than six times the average daily volume, because “sales dipped in the latest quarter and fell short of Wall Street expectations” – CNN Money, April 25, 2013, The supermarket that’s sending investors running.

“Safeway and other traditional grocery store operators continue to face secular challenges that make it difficult to improve their competitive position in food retailing.” Those challenges include competition from large retailers that offer broader sets of products and services to customers in addition to groceries. Target is at the top of this list of competitors after it has aggressively expanded food offerings. – Morningstar, quoted in ibid, The Wall Street Journal.

Our view is somewhat different. We’ve seldom owned the stock (please see Exhibit 4 below, Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason) and we would have been sold out at our stop/loss price of $24 (please see Exhibit 1 above) but there was no incentive for us to quickly buy it in January and February as its stock price shot up +40% since $18 in December. However, it’s still eligible for inclusion in the Perpetual Bond™ at prices above the Risk Price (SF) of $20 and we can keep an eye on it at these prices, or, more aggressively, buy the cheap May calls at $24 for $0.50 today. (Even the market has to eat fresh fruit and vegetables, eventually.) The company pays a dividend of $170 million per year to its shareholders for a current yield of better than 3%.

(B)(N) SWY Safeway Incorporated – Risk Price Chart – April 2013

Safeway Incorporated operates a retail food and drug chain in the U.S. and Canada and has annual sales in excess of $40 billion per year, and manages to juggle a debt burden of about $12 billion against the shareholders equity of $3 billion, inventory of $2.5 billion (suggesting a better than monthly turn) and stores and other equipment of $9 billion, net of an accumulated depreciation expense of $12 billion.

(Please Click on the Chart to make it larger if required.)

The Company also has a network of distribution, manufacturing, and food processing facilities, and owns a majority interest in Blackhawk Network Holdings Incorporated, which is a leading prepaid payment network utilizing proprietary technology to offer a broad range of gift cards, other prepaid products and payment services in the United States and eighteen other countries.

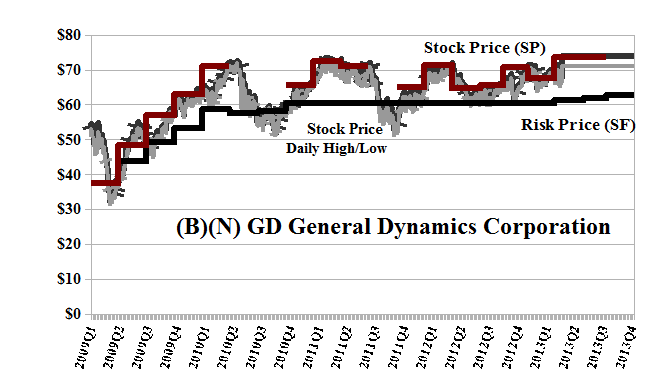

Exhibit 5: (B)(N) GD General Dynamics Corporation – Risk Price Chart

General Dynamics is one of the largest defense contractors in the United States, and one of the primary arms merchants to the world, which is a very competitive business but does not appear to be a “shrinking” . It builds the Abrams tank in Lima, Ohio, implements mobile communications systems, and owns the Gulfstream Aerospace Corporation, which is a renowned manufacturer of high-end private and corporate jets. It’s been in the Perpetual Bond™ since $65 in 2011 and the current stop/loss price is $63 which is still above the current Risk Price (SF) of $60 and rising (please see Exhibit 1 and Exhibit 5 below). It also pays a dividend of $800 million a year to its shareholders for a current yield of 3% and we’d be interested in “collaring” the stock price at between $70 and $75 through August, which we can do for a gain of $0.50 per share today.

(B)(N) GD General Dynamics Corporation – Risk Price Chart – April 2013

General Dynamics Corporation offers a broad portfolio of products and services in business aviation, combat vehicles, weapons systems and munitions; military and commercial shipbuilding; and communications and information technology, including hardened military mobile communications and information systems units which, one would think, could also be adapted to recreational uses and complement the Gulfstream aircraft.

(Please Click on the Chart to make it larger if required.)

Exhibit 6: (B)(N) LMT Lockheed Martin Corporation – Risk Price Chart

The Lockheed Martin Corporation is also a huge supplier of arms to the U.S. military and countries overseas, with about 80% of its revenues of nearly $50 billion per year coming from the U.S. government, including sales of information technology, missiles (which are not reusable), and fire control units.

In addition, the company pays a dividend of $1.5 billion per year to its shareholders for a current yield of 4.7% and its been in the Perpetual Bond™ since the much lower prices of $80 in 2011, more than two years ago. We can afford the current stop/loss price of $91, but the Risk Price (SF) is still quite low at $82 and rising (please see Exhibit 1 and Exhibit 6 below) which suggests that we should implement a “collar” on the stock price such as the December put at $90 for $3.40 per share offset by a sold or short call on our long position at $100 which we can sell for $3.60 today, although the stock price is over $98 today, and we could be called sooner than we might like, but there are obvious remedies in different terms and different strike prices that we can pay for with a small fraction of our current profits.

(B)(N) LMT Lockheed Martin Corporation – Risk Price Chart – April 2013

Lockheed Martin Corporation is a security and aerospace company engaged in the research, design, development, manufacture, integration, and maintenance of advanced technology systems and products.

(Please Click on the Chart to make it larger if required.)

And In Conclusion

We need the news, we love the news, but we can’t afford to pay any attention to it other than to check our positions in a defensive mode.

By relying on these apparently sensible “factual” assessments and effusions of investment righteousness, investors will repeat the mistake that legions of well-heeled professional investors made with Apple Computer (or Cisco and Nortel, in the day) – it was headed for $700, then $1,000, and the most valuable company in the world, ever, they say – of confusing guts, glory, and a good story, all of which could be true, but might not have anything to do with a “stock price”.

We can call our broker to find out what a stock price might be, subject to some haggling, or check the bid and ask prices, or accept the market price (which is indefinite most of the time) for small orders, but all that is known in over 100 years of trying to forecast or anticipate stock prices, is how to calculate the stock price that is consistent with “the demonstrated societal standards of risk aversion and bargaining practice” which can be shown, in mathematics and economics, to be consistent with a Nash Equilibrium between “risk seeking” and “risk averse” investors (Goetze 2009).

Please see our Posts on The Price of Risk, August 2012, and The Nash Equilibrium & Its Stock Price, October 2012, and the more recent Post, Earnings Don’t Matter, April 2013, for a simple method to test the well-known theories that don’t work.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.