(B)(N) NVDA Nvidia Corporation

Drama. The Nvidia Corporation designs, manufactures, and markets the specialized semiconductor chips and microprocessors that we use every day, invisibly and magically, to project “bits” to “clips”, numbers, text, and spreadsheets to our telephones and computer screens. The market capitalization is $8 billion and that’s about $3 billion less than it would take to buy the whole company and take it private. But, then, who will run it more effectively than the current management, many of whom, including the CEO Mr. Jen-Hsun Huang, have been there from the beginning? The total assets are $6.4 billion and the shareholders equity is $4.8 billion, and they pay a dividend of $0.08 per share per quarter or $185 million per year to the shareholders for a current yield of 2.3%.

But that’s not enough for some investors who crunch the numbers (on their computer screens) and demand to be paid forward – they want a life time of profits, now, and one way to get them is to “outsmart” the market (Reuters, March 29, 2013, More trouble for Cohen’s SAC Capital as Steinberg indicted in NY). Well, we can’t help them with that, because, after all, their profits would be our losses, and we play the game the other way with “hedge funds” that don’t know anything, and, if the numbers aren’t working out for them, are willing to “risk” a life time of free lunches courtesy of the Federal Corrections Service which, alas, we are also expected to pay for from the profits of our efforts.

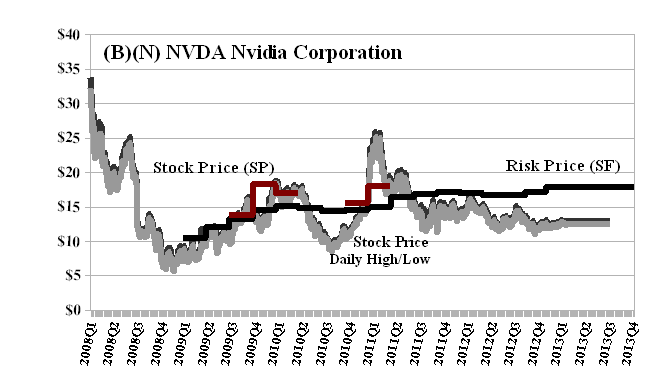

We’ve seldom had an opportunity to buy and hold the stock of Nvidia (please see Exhibit 1 below, Red Line Stock Price (SP) above the Black Line Risk Price (SF)) and in the last five years, the stock price has ranged between $30 and $6, and is currently $13 which is $5 below the current Risk Price (SF) of $18. If we were really interested in the 2.3% dividend yield, we could buy the stock at $13 and put in the stop/loss at $12 because our best estimate of the downside volatility in the stock price is minus ($1) (please see our Post, Popoviciu’s Volatility, October 2012). Alternatively, we could “collar” the stock price for the next several months by buying the June put at $13 for $0.80 per share today and selling or shorting the June call at $14 for $0.25 per share, so that for a cost of $13 per share and the collar at $0.55 per share ($0.80 less $0.25), we would be holding the stock between no less than $13 and no more than $14 until June, while we think about it, collect our dividends, and wait for more information.

The Risk Price (SF) is our best estimate of the “price of risk” which is the least stock price at which investors have demonstrated a determination to buy and hold the stock at prices above the price of risk. It is also the stock price at which a Nash Equilibrium is established between “risk seeking” and “risk averse” investors. Please see our Posts, The Price of Risk, August 2012, and The Nash Equilibrium & Its Stock Price, October 2012, for more information.

It’s because we know “where we are”, so to speak, and are “risk averse” – we want to keep our money and obtain a hopeful but not necessarily guaranteed return above the rate of inflation – that we can buy and hold with confidence, whereas “risk seeking” investors are typically driven by transient factors (such as an earnings report) and “statistics” which can be said to predict the past but seldom now. They could be right but when will that be? Please see our Post, The Dow Transports, March 2013, for an example of “risk averse” investing that has returned +28% plus dividends so far this year, and can’t be less for the rest of the year.

Exhibit 1: (B)(N) NVDA Nvidia Corporation – Risk Price Chart

NVIDIA Corporation is engaged in creating the graphics chips used in personal computers that bring games and home movies to life. It has two reporting segments: the GPU business and the between Tegra Processor business.

(Please Click on the Chart to make it larger if required.)

The GPU segment offers GeForce for consumer desktop and notebook PCs; Quadro for professional workstations; Tesla for supercomputing servers and workstations; GRID Graphics Modules for industry-standard servers to accelerate virtual desktop infrastructure; and GRID Systems for applications ranging from streaming games to hosting graphics-intensive design applications. The Tegra Processors segment offers Tegra processor, a system-on-a-chip that provides visual and multimedia experience on tablets, smartphones, and gaming devices; Icera baseband processors and radio frequency transceivers for mobile connectivity; integrated chip solutions, which combine the Tegra applications processor and the Icera baseband processor; Project SHIELD, an Android gaming device that help users enjoy digital content in the cloud; Tegra VCM, a Tegra-based vehicle computing module, which integrates an entire automotive computer into a single component; and embedded computing platforms for various digital consumer devices, such as TVs and smart monitors. The company sells its products to original equipment manufacturers, original design manufacturers, system builders, add-in card and motherboard manufacturers, and consumer electronics companies, as well as gamers, enterprises, and tablet and mobile phone users. NVIDIA Corporation was founded in 1993 and is head quartered in Santa Clara, California.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.