The Dow Transports

Drama. The Perpetual Bond™ of just the twenty Dow Transportation Companies has returned a staggering +28% since December but, as has been famously said, we didn’t do it alone. The Dow Jones Transportation Index is itself up by +18% and is widely regarded as a harbinger of “business activity” and the Dow Jones Industrial Index is also up by +10% so far this year. But new heights seem to disturb “risk seeking” investors who, justifiably, can not believe their “good fortune”, not knowing whence it comes or where it’s going because mere “volatility” investing and “diversification” by negative correlations of “risk-adjusted expected returns” describes the past but not the future, and unlikely, tomorrow or next week.

In contrast, there are twelve companies from the Dow Transports (of twenty companies) that have been in the Perpetual Bond™ since at least September of last year and are in the Perpetual Bond™ now, and we know exactly how they got there and when and how they will be leaving. Please see Exhibit 1 and 2 below.

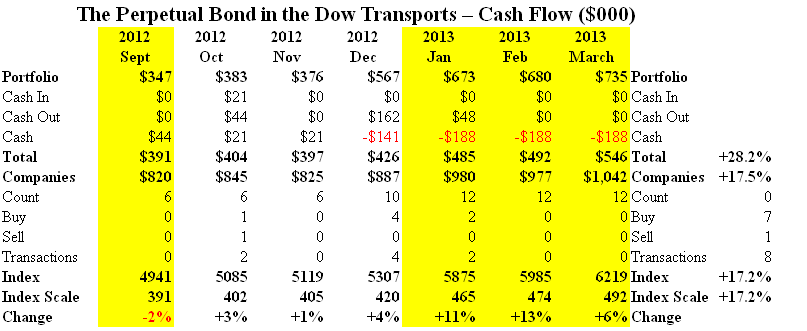

Exhibit 1: The Perpetual Bond™ in the Dow Transports – Cash Flow Summary

(Please Click on the Chart to make it larger if required.)

The Cash Flow Summary (Exhibit 1 above) is our standard high-level and simplified summary of the portfolio activity – what we bought, held or sold at the indicated prices (please see Exhibit 2 below for the companies that are in the portfolio and when) – but it does not include the details of the actual transactions, transaction costs, and the dividend earnings as they come. However, we generally buy and hold at the market price whenever a company becomes eligible for the portfolio, that is, when the ambient stock price appears to be at or above the Risk Price (SF) which is always accurate and our best estimate of the current “price of risk”. Selling is more difficult because in some cases we are sold out at the stop/loss price (please see $Stop/Loss in Exhibit 2 below) or we extend our holding time by “collaring” the current stock price (please see any of the (B)(N)-Company Posts for examples).

The Cash Flow Summary is based on blocks of 1,000 shares at the market prices so that in September, for example, the portfolio had only six companies in it (Count Line) with a market value of $347,000 (Portfolio Line) and a Cash Account of $44,000 (Cash Line). The “Companies” Line shows the value of all the companies in the Dow Transports at the same time and is a portfolio that simply buys and holds all the companies, all of the time. Its return is +20.4% since December whereas the portfolio return of the Perpetual Bond™ is +28.2% since December (Total Line which includes changes in the Cash Account due to buying and selling). Negative entries in the Cash Account indicate buying on margin which is not required but a convenience, and the Count, Buy, and Sell lines show the portfolio size and how many companies we bought or sold during that month.

Exhibit 2: The Perpetual Bond™ in the Dow Transports – Portfolio Summary

(Please Click on the Chart to make it larger, and again, if required.)

A company is in the Perpetual Bond™ if and only if the ambient stock prices appear to be at or above the Risk Price (SF) (shown as March (SF) in Exhibit 2 but may vary from quarter-to-quarter as new balance sheet information becomes generally available) and these are marked as a (B); all the others are marked as (N) and a company enters the portfolio on an (N)- to (B)-transition and leaves the portfolio on a (B)- to (N)-transition using our usual “selling discipline”.

The $GAP is the difference between the current stock price and the Risk Price (SF) and will be positive if the company is a (B) but can be negative if the price is “collared”. The Delta is our estimate of the stock price volatility (please see our Post, Popoviciu’s Volatility, October 2012) and is used to set the $Stop/Loss Price. We note that if the entire portfolio is sold at the $Stop/Loss prices (which is unlikely) then its value decreases from $735,000 to $671,000 for a minus (9%) loss.

We also note that the market value of all the companies that are in the current portfolio is $183 billion and that the portfolio “scales” without change in the strategy; in effect, $567 million in at the end of December is now worth $735 million (plus dividends) and can’t be less (with reasonable attention) for rest of the year and could still be more – which should pay some bills, would it not.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.