(B)(N) JPM JP Morgan Chase & Company

Drama. The two largest and fabled American Banks, the JP Morgan Chase & Company and the Bank of America Corporation, have been stock market phenomena for the past two years (please see Exhibit 1 and 2 below) and also the subject of many regulatory and Congressional hearings and investigations which, like teflon and The 2nd Estate, they have shrugged off with plausible explanations of “What else could we do?” (Reuters, March 15, 2013, Ex-JPMorgan executive tries to dodge harpoon of “whale” losses) and (without prejudice) we have to agree with them, that they did nothing wrong within the rules and regulations of the time. Rusty or tarnished armour is, of course, not a crime (The Exchange, October 24, 2012, On Wall Street, Selling Fear Is Good Business) and managing $2 trillion of other peoples money in the fluttering fabrics of the world economy, is not an easy task, and should they drop $5 billion here or there, blinded by their hedges, armour and helmets of statistically correct risk protection software, well, it’s their money, isn’t it, and just a charge on profits. (Please see any of ourPosts on Hedge Funds Bushwhacked By Volatility or Volatility For the Delta Challenged, June 2012.)

Because of our usual investment prudence – it’s our money, isn’t it – we missed a lot of the drama and also a lot of the profits for those investors who were prescient enough, or lucky enough, to load up on these stocks a year ago at much lower prices (JPM from $30 in 2009 to $50 now, and BAC from $6 to $13 or so, and, really, nothing has changed. Please see below.). But, we’re back now as both of these stocks are trading at or above the “price of risk” which we estimate as the Risk Price (SF) (JPM $41 and rising to possibly $43 and BAC $11 and rising to possibly $12).

We have a rule, law and regulation, too – The One Rule – we only buy or hold a stock if the stock price is plausibly trading at or above the “price of risk” and, otherwise, not (please see almost any of (B)(N) posts for more information and examples). JP Morgan is trading at $50 today and our estimate of the downside risk due to demonstrated stock price volatility is minus ($5) (please see our Post, Popoviciu’s Volatility, October 2012) so that we could be “stopped out” at $45 before we know it. A better alternative for us is to buy the stock at $50 and the June put at $48 for $1.34 per share with an offsetting short or sold call at $53 for $0.90 per share so that for a net cost of $50 per share for our long position and the options at $0.44 per share ($1.34 less $0.90), we can collect our dividends of $0.30 per share per quarter for a current yield of 2.4% and wait to see what happens next. Will we be “called out” at $53, or will the stock price drop to $48 or less and we can “put” our put at $48 if we want to.

Exhibit 1: (B)(N) JPM JP Morgan Chase & Company – Risk Price Chart

JP Morgan Chase & Company is a global financial services firm and banking institutions in the United States of America with operations worldwide.

(Please Click on the Chart to make it larger if required.)

The total assets under management exceed $2.3 trillion and have grown by $400 billion since 2009. The shareholders equity is $200 billion (or 1/10th of what they manage and owe) and that has also grown by $50 billion since 2009. The current dividend is $0.30 per share per quarter for a gigantic payout of $4.5 billion per year and a current yield of 2.4%.

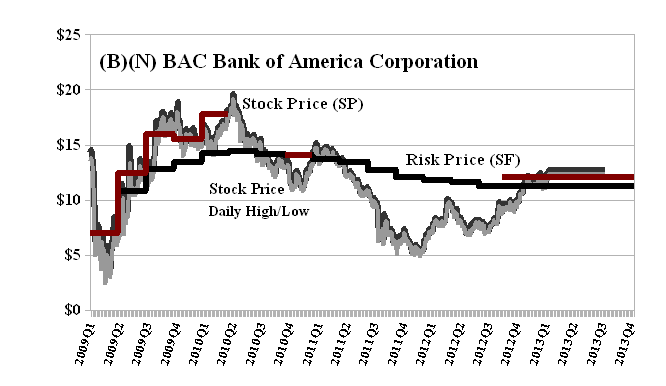

Exhibit 2: (B)(N) BAC Bank of America Corporation – Risk Price Chart

Bank of America Corporation is a bank holding and a financial holding company which through its subsidiaries, provides banking and non-banking financial services and products throughout the United States and in selected international markets.

(Please Click on the Chart to make it larger if required.)

The total assets under management exceed $2.2 trillion and that is up by $500 billion since 2009 and the shareholders equity has diminished (a little) from $260 billion in 2009 to the current $240 billion.

The situation of the Bank of America is somewhat different from that of JP Morgan. The current dividend is $0.01 (1¢) per share per quarter for an annual payout of $430 million and a current yield of 0.3%, but it’s also hard to argue with a 100% increase in the stock price since this time last year. The current downside due to stock price volatility is minus ($1.50) so that we could be sold out at $11 if we buy the stock today for $12.50. On the other hand, a bought put in June at $12 sells for $0.45 per share today and a sold or short call at $13 for $0.50 so that net cost of our stock is $12.45 ($0.45 less $0.50 which is negative) plus transaction costs. For that price, we get to see how this unfolds, and the sold call at $13 can be rolled over or bought back if the stock price continues to perform, or we can just buy the stock and buy the put and pay our $13 now.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.