Standard & Poor’s Double AA’s Down

Drama. The US Department of Justice, sixteen states and the District of Columbia are taking on the bond rating service, Standard & Poor’s, alleging fraud and malfeasance in rating trillions of dollars of mortgage-backed securities in yet more fallout from a decade of excess about to yield a decade of drama (Reuters, February 5, 2013, U.S. government slams S&P with $5 billion fraud lawsuit).

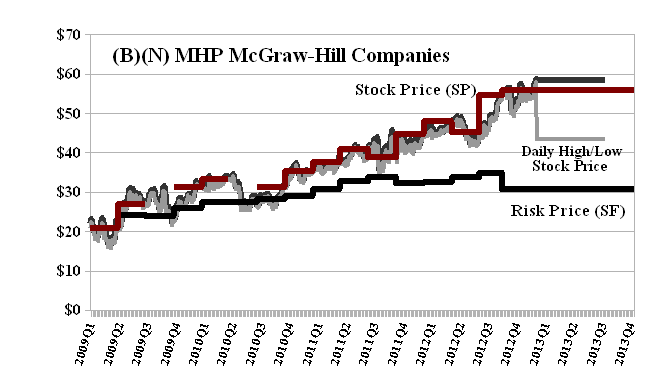

Predictably, the stock price of McGraw-Hill Companies, the hapless parent of the number-crunching kids at Standard & Poor’s, took a beating for a one day drop of $7 per share or 15% to close at $45 and over thirty million shares (about 10% of the common shares outstanding) were sold and, of course, bought by someone else in the free fall that would have been even farther had they not (please see Exhibit 1 below).

Exhibit 1: (B)(N) MHP McGraw-Hill Companies – Risk Price Chart

McGraw-Hill Companies Incorporated is a global information services provider serving the education, financial services and business information markets with a range of information products and services.

(Please Click on the Chart to make it larger if required.)

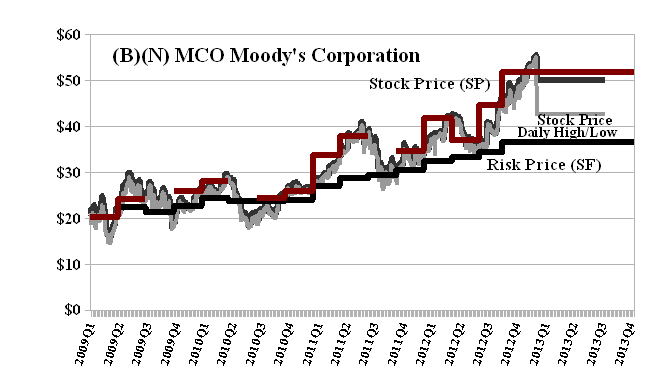

Both S&P and their ranking comrade, Moody’s Corporation, have been in the Perpetual Bond™ since 2010 and we started buying them at much lower prices (please see Exhibit 1 and 2 below, Red Line above the Black Line) and with our usual stop/loss and “safety first” provisions (please see almost any of these Posts or The Wall Street Put, August 2012 and (B)(N) MCO Moody’s Corporation, December 2012) were indifferent to this latest accident. Nor are we buying them now at these fire sale prices which knocked off about $2 billion from the market value of Moody’s and a similar amount from S&P pending new balance sheet information and the further relaxation of investor angst. Between Monday’s prices and today’s and the volumes of about thirty million shares traded in each company, investors left more than $500 million on the table as they rushed for the exit.

Exhibit 2: (B)(N) MCO Moody’s Corporation – Risk Price Chart

Moody’s Corporation is a provider of credit ratings, credit and economic related research, data and analytical tools, risk management software and quantitative credit risk measures, credit portfolio management solutions and training services.

(Please Click on the Chart to make it larger if required.)

But that’s the point, isn’t it. Investors buy bonds with low ratings because they are prepared for losses in the hope of higher gains. Stock prices are the same and the watershed price is the “price of risk”. For more on this, please see our Posts, The Price of Risk, August 2012 or The Nash Equilibrium & Its Stock Price, October 2012.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.