(B)(N) AAPL Apple Incorporated

Drama. We thought that we were done with Apple Incorporated (please see our previous Posts and December 2012). Great products (they say), great marketing, great margins – iThings “apps” and “snaps”, so to speak, that for a time made it the most valuable company in the world in terms of its market capitalization which was as high as nearly $700 billion four months ago and significantly up from $70 billion in 2007 (just five years ago) and $2 billion in 1985. If Rip Van Winkle had just bought 1,000 shares for $2,000 in 1985, he would have woken up to a fortune of $700,000 last year rather than the current rather tawdry $460,000 although many analysts were suggesting that he should hold out for $1,000,000 this year (Reuters, January 30, 2013, The funds that saw Apple’s decline coming). Does that mean he should buy more or keep $460,000 worth now and go back to sleep?

Of the hundreds of popular mutual funds with a significant stake in Apple stock amounting to more than 5% of their assets and billions of dollars, less than 20% of them – one in five – did anything at all last year, like take some profits and thank their good fortune, or, for a few dollars more, protect their prices (please see our Post, The Wall Street Put, August 2012) and be grateful later, and if it weren’t for enough buyers at the current $450, the price would even be lower. And who knows how low. It’s just a fact that all stock prices begin and end at zero (even in an acquisition when the stock price becomes the new owner’s opportunity or problem) and what’s a company with a dull glow and lots of very competent competition going to be worth next year? Some people say it has lots of cash but, then, so do we and our first goal in investing is to protect our cash cum capital – 100% Capital Safety and a hopeful return above the rate of inflation – and that takes more than just gambling on the latest great story which only works until the surprise ending.

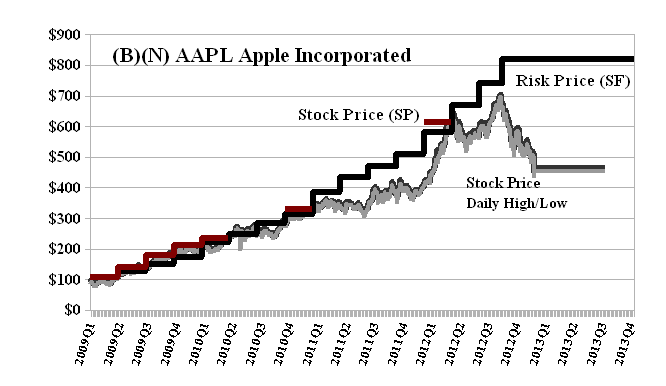

Apple Incorporated has not been signalled as a buy or hold for the Perpetual Bond™ since early 2011 at $350 when we respected what we knew rather than bet on what we didn’t and sold the last of our holdings (please see Exhibit 1 below) without regrets that had we waited and bet on the future, we might have doubled our money again and not merely tripled it. Oh well.

Exhibit 1: (B)(N) AAPL Apple Incorporated – Risk Price Chart

Apple Incorporated designs, manufactures, and markets personal computers, mobile communication devices, and portable digital music and video players and sells a variety of related software, services, peripherals, and networking solutions.

(Please Click on the Chart to make it larger if required.)

We only buy or hold a stock if the ambient stock prices as represented by the Stock Price (SP) (Red Line, a step-function in Exhibit 1) appear to be at or above the “price of risk” or Risk Price (SF) (Black Line) which is also a step-function updated at most quarterly as new balance sheet information becomes generally available (please see our Post, The Price of Risk, August 2012, or almost any of these Posts for more examples). The price of risk is provably “the least stock price at which a company is likeable” (Goetze 2009) and “likeability” is not just a pretty picture but the demonstration that investors with a strong sense of risk aversion are committed to buying and holding this stock at those prices, and otherwise not.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

…