The New Voodoo of Investment Theory

Essay. Why does the moon not fall down and crush us? The ancients and not even the Romans, didn’t know why and when the Harvest Moon was big and bright and looming close on the horizon – full and expectant so it seemed – it seemed wise to offer food, drink and celebration. And that seemed to work.

The pillars of finance that currently animate the Comptroller’s Office of the City of New York are also looking for “things that seem to work”. Their plan is to avoid the often touted “long-short funds” (for good reason one would think – please see our Post, Hedge Funds Bushwhacked By Volatility, November 2012) and go for the latest technology and practices in “event-driven” hedge fund managers who can predict triggers for stocks and bonds such as corporate restructuring, acquisitions, management changes and share sales AND “commodity trading advisers” who buy and sell commodity linked and other futures AND “macro funds” which bet on global economic trends AND “relative- value” strategies that attempt to profit from price differences between assets.

Nor are they alone in contemplating this celebration of promising ideas and new “investment products”. It appears that two pension plans in San Jose, California and the Kentucky Retirement Systems are also allocating capital to hedge funds in order to diversify investments, dampen volatility and improve returns (Bloomberg, December 18, 2012, New York Pensions to Add Hedge Funds to Reduce Volatility) and the Nobel Foundation is another notable that is looking for new solutions to the persistent and frightening problem of low or negative returns and the uncertainty of not knowing what will happen next (please see our Post, The Shire Green, December 2012).

In addition to all of that, we shall have “dancing” because the perception is that “smaller” managers who are emerging and managing less than $1 billion can be more nimble and flexible and not merely slaves to old and dated technologies that are freighted with too much money. One might regard King David in that context and, indeed, the “Four Horsemen” already mentioned are already out there and their results have been and are being regularly and systematically compiled by UCITS (Undertakings for Collective Investment in Transferable Securities) and Hedge Fund Research Incorporated (HFRI) under the exact rubrics that we are looking for (please see Exhibit 1 below).

Exhibit 1: UCITS and HFRI Indicative Data – Not Approved for General Use

HFRU Index Summary – The New Voodoo File

(Please Click on the Chart to make it larger if required.)

We’re cautious, of course, in interpreting these data. The Summary Line (HFRU/UCITS Hedge Fund Composite Index) appears to indicate a +4.87% gain last year but a minus (-3.89%) loss the year before and the four hopeful investment “styles”, so to speak, show a similar lack of productivity and muted variability or volatility and we have also studied the “dancers” in an earlier post, The Active Investor (DOA), November 2012.

We are simply not used to looking at such odd data in the context of positive returns and reduced volatility. And we don’t think that the moon is falling down and we are happy with our investments that try to do only one thing – 100% Capital Safety guaranteed and a hopeful (but not guaranteed) return above the rate of inflation. So, for example, the S&P 500 NYSE Perpetual Bond™ returned a +20% gain on capital last year plus another 2% or 3% of dividends by simply managing an ordinary portfolio of the stocks in about two hundred companies and, of course, we used our usual buying and selling disciplines (please see our Post, The Wall Street Put, August 2012) in order to protect our gains and prices (should we have any) year after year, again and again, because we know exactly how that is done. No guessing! No forecasts! No fear!

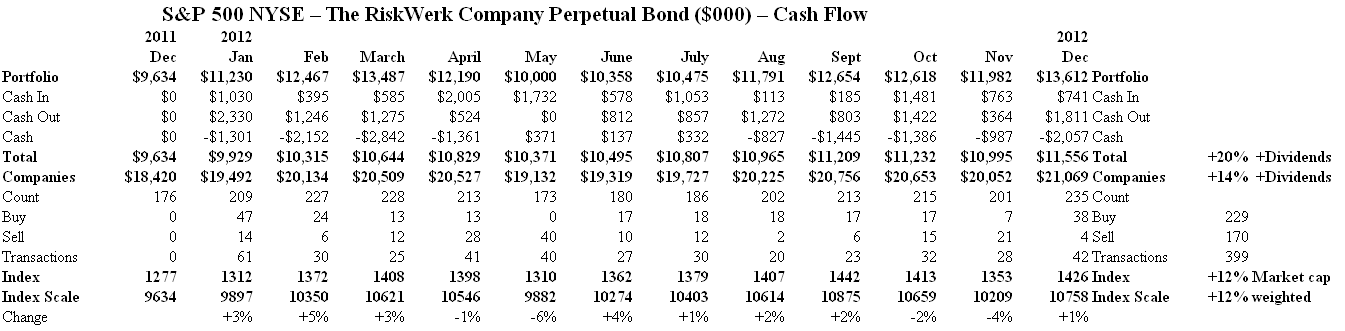

Exhibit 2: S&P 500 NYSE – The RiskWerk Company Perpetual Bond – Cash Flow

S&P 500 NYSE – Cash Flow

(Please Click on the Chart to make it larger and again if required.)

The Cash Flow Chart is our standard chart and has been described in many of our Posts. For example, the above Chart shows that we invested $9,634,000 in late December 2011 and early January 2012 by buying uniformly blocks of 1,000 shares in 176 companies (as opposed to $18,420,000 if we had bought similar blocks in them all). The market Perpetual Bond™ is an actively managed portfolio of stocks and our buying and selling activity is shown in the monthly Count, Buy and Sell lines. At the end of December 2012, the portfolio was worth $13,612,000 with 235 companies in it and a margin account (optional) of $2,057,000 for a net Total of $11,556,000 should we chose to retire the margin account. The portfolio obviously “scales” in the $11 trillion market of the S&P 500 NYSE and $10 million could just as well have been $100 million or $100 billion without creating any “tidal” waves, so to speak.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.