(B)(N) ABX Barrick Gold Corporation

Deal Book. The Barrick Gold Corporation has terminated its early stage talks to sell its substantial (74%) interest in the African Barrick Gold Company to the state-owned China National Gold Company (Reuters, January 8,2013, Barrick ends talks to sell African unit to Chinese buyer). Barrick’s asking price of around $3 billion for all of the Tanzanian-based gold mining company (which has a number of operational and production challenges) is not an overly significant amount of money for Barrick Gold which has a current market value of $35 billion or $35 per share, total assets in excess of $52 billion and net worth or shareholders equity of $25 billion and also paid $800 million in dividends to the shareholders last year ($0.80 per share for a current yield of 2.4%). On the other hand, Barrick Gold (which is said to be the world’s largest gold producer) lost more than 20% ($15 billion) of its market value last year and is presently trading at a substantial discount to its Risk Price (SF) which we estimate at $63 (please see Exhibit 1 below) and has a further downside risk due to volatility of minus ($5) or nearly 15% of its current stock price.

Until it earns its risk price, the company is in the trading zone (N) of stock price volatility and investor uncertainty animated by investor opportunism (greed) or pessimism (fear). The Risk Price (SF) is also a defensible “takeover” price for someone who wants to buy the whole company ($63 billion at $63 per share) which is unlikely as an all cash deal (although one never knows) but has implications for cash plus stock deals (please see, for example, (B)(N) IMN Inmet Mining Corporation, November 2012, and other Posts in the Deal Book).

Exhibit 1: (B)(N) ABX Barrick Gold Corporation – Risk Price Chart

Barrick Gold Corporation is engaged in the production of gold, exploration and mine development and is the world’s largest gold producer with an output of 7.7 million ounces in 2011.

(Please Click on the Chart to make it larger if required.)

Not all the major Canadian gold, silver and related resources companies are so challenged (please see Exhibit 2 below) and the sector as a whole returned a remarkable +29% plus dividends last year when managed as a Perpetual Bond™ in contrast to a simple buy and hold strategy which produced a loss of minus (-1%) and underperformed the S&P TSX Composite Index (+4%). Please see Exhibit 3 and 4 below for a more detailed summary of the industry.

Exhibit 2: (B)(N) YRI Yamana Gold Incorporated – Risk Price Chart

Yamana Gold Incorporated is a Canadian-based gold producer with significant gold production, gold development stage properties, exploration properties and land positions in Brazil, Chile, Argentina, Mexico and Colombia.

(Please Click on the Chart to make it larger if required.)

Yamana Gold is a $12 billion company (up +11% in 2012) that paid $196 million in dividends last year or $0.26 per share for a current yield of 1.6%. One sees from the Risk Price Chart (Exhibit 2 above) that Yamana was in the Perpetual Bond™ (B) at prices between $12 in early 2011 and $18 to $20 last year (Red Line which is the Stock Price (SP) at which we buy, hold or sell the stock subject to the “selling discipline” above the Black Line Risk Price (SF), both of which are step-functions typically good for the quarter). The current Risk Price (SF) is $13 and our estimate of the downside risk due to volatility is minus (-$2).

There are over seventy gold and silver (and related) mining companies in the S&P TSX but only half of those (about thirty-five companies) with a market value in excess of $1 billion (please see Exhibit 4 below). No doubt fortunes can be made or lost in the “small caps” but on balance, on a portfolio basis, we expect only random results from the small caps because it is difficult for investors to understand what these companies are actually doing and what they might accomplish in the present tense rather than in hindsight. Moreover, if we did understand what they’re doing, then it is not unreasonable to consider buying the whole company for a few hundred or so million.

Exhibit 3: S&P TSX Golds & Mining Sector – Cash Flow

(Please Click on the Chart to make it larger if required.)

The Cash Flow Chart (Exhibit 3 above) shows the Index result (+4%) and the “buy/hold” result (-1%) in which we simply buy the entire market on the basis of share prices (a notional 1,000 shares of each company) in late December 2011 and early January 2012 and hold it for the entire year. The Total Line shows the result of the same portfolio managed as a Perpetual Bond™ and the return is +29% plus dividends which will add another 2% or 3% to the returns. For example, in December 2012 we bought two companies (New Gold and Silver Wheaton) and sold one (Silver Standard) and the current portfolio has eight companies with a current market value of $231,000 (Portfolio Line) and we have a cash account deficit (or margin account) of minus ($97,000) which, of course, we can readily resolve by selling equities and the net result is $134,000 (Total Line) up +29% from $102,000 in December 2011. These results, of course, scale seamlessly in that market which is presently capitalized at $235 billion.

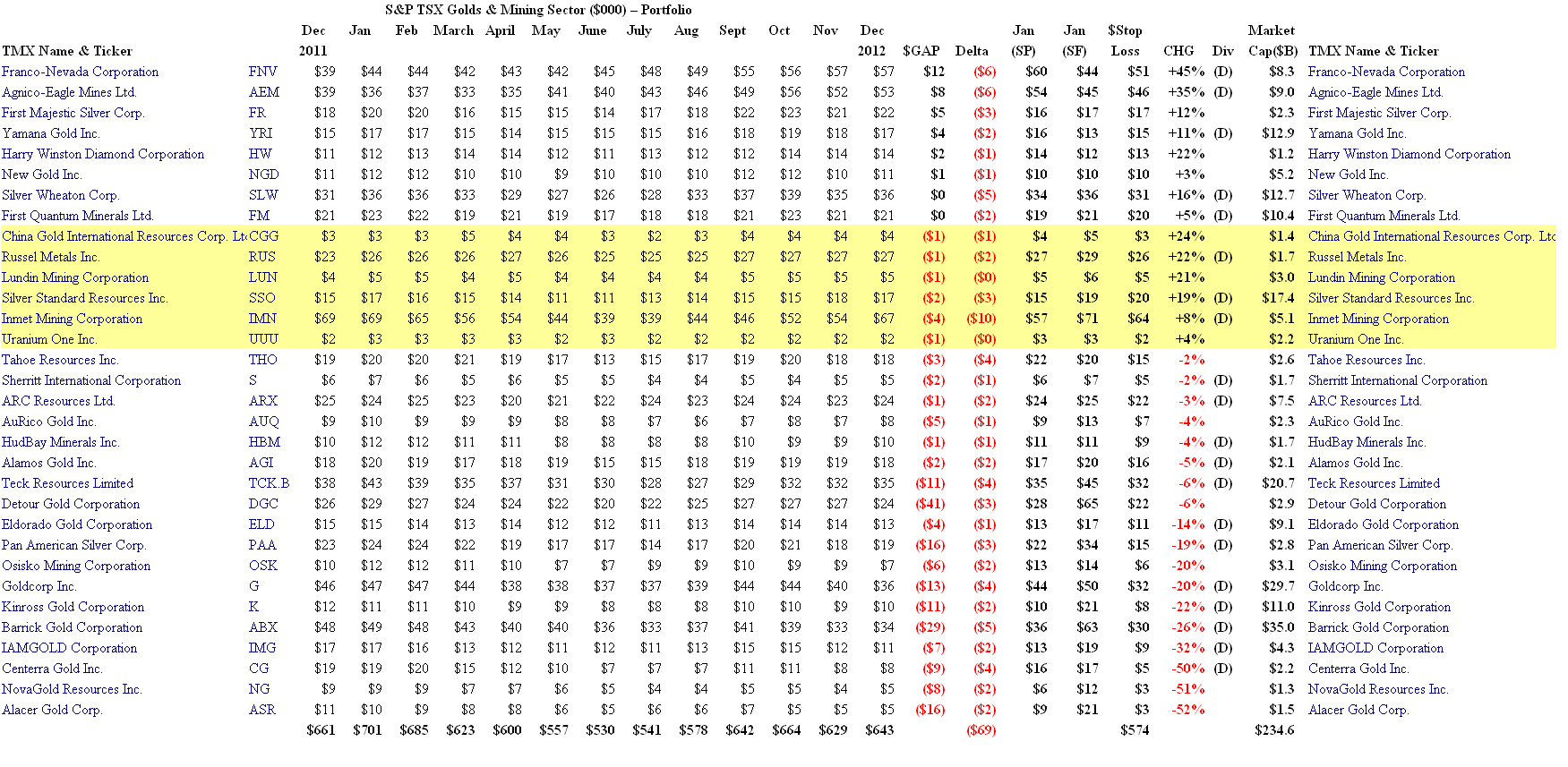

Exhibit 4: S&P TSX Golds & Mining Sector – Portfolio

(Please Click on the Chart to make it larger and again if required.)

The current portfolio (which is a Perpetual Bond™ restricted to this market of thirty-five companies) has just eight companies in it because and only because the ambient stock prices appear to be at or above the “price of risk” which we estimate from generally available balance sheets as the Risk Price (SF) (please see our Post, The Price of Risk, August 2012 or The Power Principle, December 2012, for more information). Another six companies (shown in yellow) are close because the $GAP which is the difference between the current stock prices and the Risk Price (SF) is small and, in fact, spanned by the volatility range (Delta). One might call these “a sighting” or UFO yet to be confirmed until more information in the form of current balance sheets becomes generally available. We never speculate and we never forecast or try to divine the future.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.