(B)(N) JCI Johnson Controls Incorporated

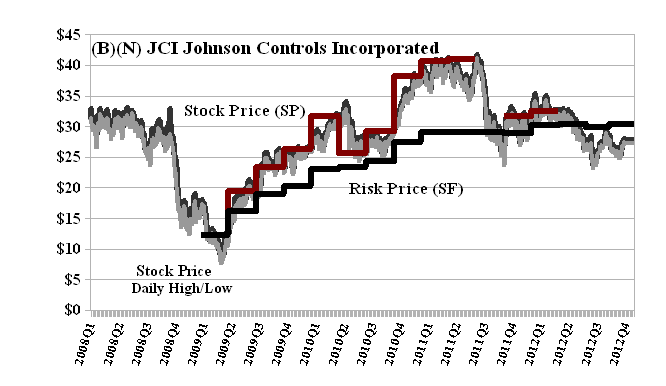

Drama. Johnson Controls has been struggling in the stock market for nearly two years and is currently down significantly since $40 in 2011 and the current $28. The current downside risk is still minus ($3) and we can’t buy it for the Perpetual Bond™ because – and only because – the ambient stock prices appear to be below the Risk Price (SF) which is $30 and has been slowly rising for the past several years (please see Exhibit 1 below) in contradistinction to the stock prices which appear to be drifting downwards in the absence of renewed investor support. The company has recently raised its dividend to $0.76 per year or $520 million per year for a current yield of about 3% which is comparable to inflation.

Does the stock price matter or tell us anything at all about now or the future? (Please see our November Post on the matter.) How “risky” can it be to buy a $28 stock with a current yield of 3% and total market value in excess of $19 billion down from $27 billion a year ago? Perhaps we’ve just answered that question but to make matters even more confusing, how does one explain how a $30 stock in 2008 became a $10 stock in 2009 (a year later) and a $40 stock two years after that and finally, again, a $30 stock even though the company itself is not materially different in all of that time and has simply grown larger in every way in a very difficult business.

The news of the day is that Johnson Controls is in a “bidding war” with the Wanxiang Group Corporation (of China) for the assets of legally bankrupt A123 Systems Incorporated (The Chicago Tribune, December 2, 2012, With both U.S. and foreign bidders, politics may come into play in Thursday’s auction of bankrupt energy-storage technology firm). The technology appears to be quite impressive and one, of course, wonders how it should go “begging”, so speak (please see below for more about A123 Systems) since the amounts of money involved appear to be in the $100’s of millions (only) and “trifling” in the context of these great companies.

The “news of the day” is thus of no help and it’s often the case – and might be expected – that the news of the day has already happened and investors can only react to it rather than be in front of it. No doubt too late for the last “guy” (investor) who bought Johnson Controls at $40 a year ago “bareback” and enthused with hope, we guess. Please see our Posts, The Wall Street Post, August 2012, and Popoviciu’s Volatility, September 2012, for the basic mechanics of “protecting” stock prices against volatility and the unknowns yet to be known and revealed only in hindsight. Too late.

In contrast, the Risk Price (SF) is enduring and its current value is written, in effect, by the investors themselves who are far less changeable than the companies and circumstances they invest in and have only one goal – save our capital and give us a hopeful return above the rate of inflation. Please see our Post, The Price of Risk, August 2012, for more information.

Exhibit 1: (B)(N) JCI Johnson Controls Incorporated – Risk Price Chart

Johnson Controls creates products, services and solutions to optimize energy and operational efficiencies of buildings, lead-acid automotive batteries and advanced batteries for hybrid and electric vehicles and the interior systems of automobiles.

(Please Click on the Chart to make it larger if required.)

A123 Systems Incorporated (Nasdaq: AONE) is a leading developer and manufacturer of advanced lithium-ion batteries and energy storage systems for transportation, electric grid and commercial applications. The company’s proprietary Nanophosphate® lithium iron phosphate technology is built on novel nanoscale materials initially developed at the Massachusetts Institute of Technology and is designed to deliver high power and energy density, increased safety and extended life. A123 leverages breakthrough technology, high-quality manufacturing and expert systems integration capabilities to deliver innovative solutions that enable customers to bring next-generation products to market.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.