The “Quintessential” Perpetual Bond

The “Quintessential Perpetual Bond” is a Perpetual (Forever) Bond™ that pays dividends and always provides a positive return on the capital (100% Capital Safety) although not necessarily against itself because the current values of the “bond” depend on the market prices and capital gains and dividends that are earned on the capital. We also hope that it provides a return that is not only positive but exceeds the rate of inflation. After all, we don’t invest in order to lose our money. We invest in order to keep our money and obtain a hopeful return above the rate of inflation, which benefits money alone cannot provide.

The Quintessential Perpetual Bond, of course, can’t really exist because it needs to deal with the reality that all stock prices begin at zero and eventually end at zero. They begin at zero or a typically small par value when issued from the treasury and authorized stock of the company and they end at zero when the company fails in bankruptcy or obsolescence or is acquired in which case the stock price becomes the problem (or, hopefully, opportunity) of the new owner. In between, the stock price is determined by, typically, tens of thousands of individually motivated investors who are buying and selling the stock to each other and each is hoping to get something more than what they paid for it.

The Perpetual Bond™ is then a managed portfolio over the long term and we will need to make buy and sell decisions eventually, but we can gain some insight into the short-term or core behaviour of the Quintessential Perpetual Bond by just buying and holding the stock of only those companies which appear to be a (B) for long periods of time (please see our Post, The Perpetual Bond (B), June 2012, for more information on how (B) and (N) are determined) and there are many of those in the current markets.

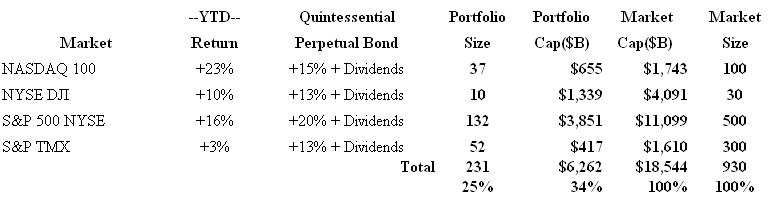

Exhibit 1: All Markets Quintessential Perpetual Bond (Nine months or more)

(Please Click on the Chart to make it larger if required.)

In the four major North American markets (please see Exhibit 1), there are about 231 companies that have been a (B) all year (nine months or more, so far) and they will remain a (B) until they become an (N). We also note that these companies represent about 25% of all the companies in those markets (930 of them) and yet have about 34% of the market value and, with the exception of the NASDAQ 100 Index, the portfolios of these companies have exceeded the market returns quite significantly and, as we noted in our recent Post, Churn, Churn, Churn, September 2012, we actually own these stocks and their dividends, and we also know when we ought to consider “selling” them, as opposed to a piece of paper with an Index number (and no dividends) that we have no hope of understanding. One can only say that the Index is what it is but we have no idea of what it might become or when.

One also begins to appreciate how fragile and competitive the capital markets for equities and the ownership of real stocks actually are. For just $30 trillion, which gives a takeover premium of 50% over the current market capitalization of $18 trillion, we can buy them all and that’s less than 3% of the $800 trillion that is floating around in the world looking for things to buy that might retain their value and beat inflation. It’s no wonder that investors are under a lot of stress. For more on this, please see our Posts, Numbers 20:12, August 2012, and The Weal of Fortune, September 2012.

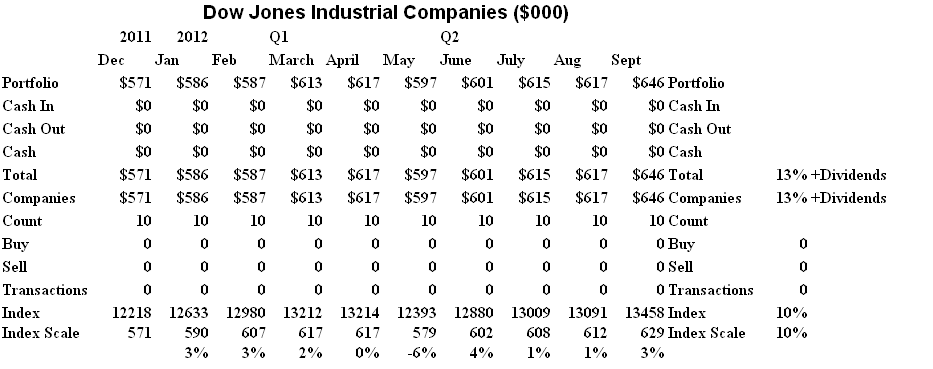

The current Quintessential Perpetual Bond in the thirty companies of the Dow Jones Industrial Companies (please see Exhibit 2 and 3 below) has returned +13% plus dividends for the year-to-date and there are no transactions required other than to buy an interest (1,000 shares in each for a total cost of $571,000 in the example) in precisely ten of the stocks (Exhibit 3) at market prices in January.

Exhibit 2: The Dow Jones Industrials “Quintessential” Perpetual Bond – Cash Flow

The Dow Jones Industrial Companies – Cash Flow Summary

(Please Click on the Chart to make it larger if required. Exhibits 2 and 3 are our standard portfolio Cash Flow Statements and the Chart elements are described in more detail in many other Posts such as Alberta & Company or (B)(N) The Nexen Best Thing, September 2012.)

Exhibit 3: The Dow Jones Industrials “Quintessential” Perpetual Bond

(N) The Dow Jones Industrial Companies")

Of course, we know which of the thirty companies are a (B) in January, and for how long they’ve been a (B), but we don’t know for how long they will remain a (B) – that’s only resolved by new balance sheets as they become generally available or by breaching the known risk price which is calculated only quarterly and based only on known data. Please see The Wall Street Put, August 2012 or Popoviciu’s Volatility, September 2012, for more information on how we protect our gains on stock prices.

Of the ten companies, only MCD McDonald’s Corporation has not had a net positive price gain so far this year (currently $93 down from $98 in January and again in March) but we note that we have owned it since $50 in early 2009 (Three years ago. Please see Exhibit 4 below.) and our only issue has been how to take profits or protect the current price against ambient volatility or corporate mishap. Our estimated downside based on the demonstrated volatility (please see our Post, Popoviciu’s Volatility, September 2012) is $5 so that a stop-loss at $98 (March) less $5 would have sold us out at $93 or less. Instead, we bought (in March) the December put at $95 for $1,900 (1,000 shares) and sold the December call at $100 for $950 and, so, for a net cost of about $1 per share we still have lots of time to make our “sell” decision and will also collect $2,900 in dividends this year. Now, that’s what we call “stress free” investing.

Exhibit 4: (B)(N) MCD McDonald’s Corporation – Price Chart

(N) MCD McDonalds Corporation")

(Please Click on the Chart to make it larger if required.)

The Dark Line and grey zone below it are the daily highs and lows of the stock price. The Red Line (a step-function) is an indicator price, Stock Price (SP), at which we might have “bought” or “sold” the stock based on the comparison with the current Risk Price (SF) (the Black Line, also a step-function). A company is a (B) if and only if the current Stock Price (SP) plausibly exceeds the current Risk Price (SF) based on the known information. “Buying” is usually quite trivial – we just buy blocks at the current market price and are not overly concerned about the market capitalization weights that seem to animate so much of investment “thinking” (please see our Post, Churn, Churn, Churn, September 21012) – but the discipline of “selling” is, generally, more difficult when large blocks are involved or we might want to just keep the stock but protect our current prices and delay a decision.

For more information, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us (for free) in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”.

Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability.

We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now.

The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.