The Canadian Bank Act

The “Canadian Bank Act” is a Perpetual Bond™ with domain consisting of the eight Federally chartered and (more or less) national banks. The RiskWerk managed portfolio of just these eight banks has returned 3% plus a 4% dividend yield so far this year and, obviously, has outperformed the S&P TSX Composite Index which has returned nothing and one sees no reason that should not be the case for the rest of the year. We’ll know, of course, in a few months but if 7% or more is good enough for us this year on just the banks then we can lock in our gains in the usual way (please see, for example, No Stock Is Forever, August 2012) and wait for Christmas.

But how do we know which banks to buy and sell and when? After all, the major banks should be just about the same – they all take deposits, make mortgage, consumer and business loans, and charge more or less the same service fees for more or less the same services. They are also all regulated in the same way and have the same capital requirements and one would think that our investments would be as safe with any of the banks as our money is in them (unless we have too much of it).

But that’s just the point. A bank needs to take care of business (please see, A Business is a Customer, September 2012) and its business is to establish and maintain useful relationships with its retail customers. Everything else, such as “investment banking” and grandiose sovereign loans, for example, is just speculation and one night stands in unregulated global markets that may compromise what they’re good at, at home. That’s just our view, of course, but tens of thousands of investors seem to share that view with measurable results that inform our investment decisions. Please see these Letters, The Price of Risk and Numbers 20:12, August 2012, the latter for more on global investing.

Exhibit 1: The Canadian Bank Act Perpetual Bond™ – Cash Flow Statement

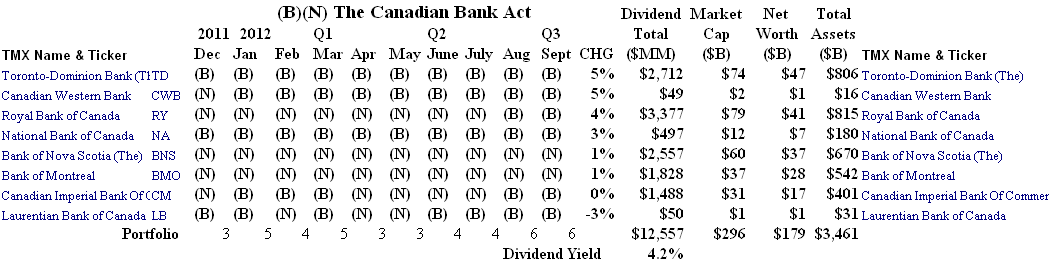

Exhibit 2: The Canadian Bank Act Perpetual Bond™ – Portfolio

(Please Click on the Reports to make them larger if required.)

These Reports (Exhibit 1 and 2) are our standard reports on the portfolio cash flow and the portfolio contents (what and when we bought and sold) and the line items are described in more detail in, for example, the recent Alberta & Company or Quebec Limited, September 2012.

One sees (Exhibit 2) that we began the year with just three of the eight banks, marked (B) (Toronto-Dominion, National and Laurentian) and presently hold six at the end of August and into early September. This year, however, we have never held the Bank of Nova Scotia or the Bank of Montreal (all marked (N)) despite a positive price gain (CHG) of +1% and expected dividends that will exceed 4% and the reason is that both banks are trading in the volatility zone (N) of investor uncertainty and won’t get into our portfolio until that is resolved and they are plausibly trading in (B).

Exhibit 3: (B)(N) BMO Bank of Montreal – Price Chart

(N) BMO Bank of Montreal - Price Chart")

The Dark Line and Grey Zone below it show the daily high/low stock prices and the Black Line, which is a step-function and changes only quarterly as new balance sheet information becomes generally available, is the calculated Risk Price (SF). The Red Line (also a step-function) shows the Stock Prices (SP) at which we nominally bought and held or “sold” the stock with our usual “selling” discipline in force (please see, for example, (B)(N) AAPL Apple Computer Inc, August 2012, for more detail on these tactics). We only buy or hold the stock if the Stock Price (SP) plausibly exceeds the Risk Price (SF) and it is, therefore, a (B) and we “sell” on a (B)- to (N)-transition, usually with a bought put on our long position that is partially offset with a sold call of similar duration at an opportunistic price (please see, The Wall Street Put, August 2012). Based on the chart, we held BMO continuously between $28 in early 2009 through $55 in late 2011 (three years later) paying no actionable attention to market volatility during that time simply because, and only because, the Stock Price (SP) plausibly exceeded the Risk Price (SF). To execute the “sale” we were sold out on our short call at $58 in early 2012 and have not bought it since and one notes that the current risk price is $60 and above the apparent “stock price”.

One could contrast the Canadian banks with the “big six” US City Banks that also provide national retail banking but have also developed a reputation for significantly “playing” their capital which, after all, does not really belong to them.

Exhibit 4: The US City Banks Perpetual Bond™ – Cash Flow Statement

The US City Banks – Cash Flow

Exhibit 5: The US City Banks Perpetual Bond™ – Portfolio

This portfolio has returned 13% plus dividends of 1.5% but we have only two or three of the six companies despite some interesting price gains, for example, BAC Bank of America, +25%, which we have been determined not to own for quite some time.

Exhibit 6: (B)(N) BAC Bank of America – Price Chart

(N) BAC Bank of America - Price Chart")

Obviously, a lot of investors thought that BAC was a bargain at $20 in late 2008 and at least some remembered to sell at $38 three months later. We bought in at $10 in early 2009 and our bought put protected the price at $18 a year later. The Stock Price (SP) then tracked the Risk Price (SF) for about a year (and we did not own it) and then dropped below the risk price in early 2011 and the risk price is also declining which “seals the deal” for us, for now and throughout 2012.

We also note (Exhibit 5) that, in addition to meagre dividends (1.5%), the total market value ($582 billion) of the six US City Banks is less than their net worth (shareholders equity $789 billion) and again less than 1/10th of the total assets ($8,200 billion – our deposits) secured or sequestered or hopefully worked thereby in contrast to the Canadian banks in which the numbers and inference is reversed (4.2%, $296 billion, and $179 billion) and $3,461 billion or twenty times the net worth at work.

For more information, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Two of our recent Letters, The Price of Risk and Maximising Shareholder Value (LOL), August 2012, may also be helpful and data may be obtained from us (for free) in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”.

Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability.

We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now.

The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.